Featured article

Monetizing underage users has always been challenging. Lower advertiser demand, stricter regulations, limited targeting capabilities, and a smaller pool of suitable advertisers all made COPPA traffic inherently more difficult to monetize compared to general or, to be more specific, “adult” audiences.

We often discuss optimization and incremental ad revenue, tweaking a floor here or adding a bidder there, and finding different hacks to squeeze out an extra 5% in ARPDAU. But for publishers with underage audiences, the conversation has shifted from "how do we optimize?" to "how do we even keep the lights on?". Until recently, this was only relevant for games that were directed to children, but the reality is that any game with a mixed audience should be worried because turning a blind eye and treating all users the same way is working until someone (Google and Apple) starts actually enforcing this.

So if we want to play by the rules and serve ads to the underage users, what are the obstacles? For starters, which mediation to use?

MAX by Applovin - Not even an option.

AppLovin implemented a restriction against serving advertisements to COPPA users, effective January 2025. To make sure that publishers bear all the responsibility and potential consequences, they announced that it will be prohibited to initialize Applovin’s SDK for users under the age of 13. Full policy is listed under Prohibition on Using the Services in Connection with “Children” or Apps Exclusively Targeted to “Children“.

However, this isn't just a loss of one network; it’s a platform-level block. If your game relies on MAX and you have users flagged as underage, this means that you cannot request an ad from MAX mediation (and all networks used with it). Because of this, publishers that were collecting users’ age and sharing that information with Applovin and other networks through MAX had to stop serving ads through MAX to users below the age of 13.

These publishers had to start using another mediation for COPPA users, or stop serving ads to them altogether.

AdMob by Google - Maybe, but for how long?

Though many turn to AdMob mediation if they have a significant portion of COPPA users, due to their ads being the most user-friendly, there is a catch. In an almost completely bidding environment, AdMob said: No bidding for COPPA users.

While the rest of the industry has spent the last two years moving toward a "Bidding-Only" world to “reduce latency and increase competition”, on AdMob, COPPA traffic is stuck in the past. AdMob requires publishers to use traditional waterfalls for these users. The only exception is the AdMob network itself, which always works as a bidder on AdMob mediation.

This is a ticking time bomb. Many of the industry’s top-performing ad networks have pivoted to being bidding-only. By forcing COPPA users into a waterfall-only structure, you are effectively locked out of a huge portion of demand that was coming from the major players that moved to bidding-only. You are left fighting for the scraps of the few networks that still support legacy waterfalls and hoping that their waterfall instances will live to see another day.

Fairbid by DT - It works, but…

Fairbid can serve ads to COPPA users regularly. However, they support fewer ad networks compared to other mediations, and their mediation/waterfall management is a bit more complicated and demanding. Besides, according to our research from a year ago, the market share of their mediation is way below MAX, LevelPlay, and AdMob.

LevelPlay by Unity - The only solution without restrictions.

LevelPlay could actually become the leading mediation for COPPA users. They support all COPPA-compliant ad networks (through official or custom adapters) and bidding. When you add the AdQuality tool being there by default, it makes things even better.

What about the ad networks?

April 30th, 2026, marked a significant turning point with the deprecation of ironSource Direct.

For years, ironSource was one of the reliable networks for COPPA demand. While the IronSource Exchange is still available for a general audience. However, COPPA users won’t be getting any impressions from ironSource Exchange since it was never delivering ads to them in the first place. Effectively, if you are a COPPA publisher on AdMob, DT, or some other mediation, you can safely remove the ironSource SDK adapter, as it will not be delivering any ads at all anymore.

Without ironSource Direct, the pool of available ad networks has shrunk from a small pond to a puddle. When you subtract the networks that have gone bidding-only and the networks that have exited the COPPA space due to compliance fears, there are very few players left on the field. Not to mention that if you need to be compliant with Google Play’s Families Policy, the list of available networks is even shorter. These are some of the main networks used for the COPPA audience:

- Kidoz - Custom adapter on AdMob; Performance on Unity’s LevelPlay is not always as good as with the direct integration.

- SuperAwesome - Same as Kidoz.

- UnityAds - Problematic on AdMob since it’s bidding-only.

- Liftoff Monetize

- DT Exchange

- InMobi

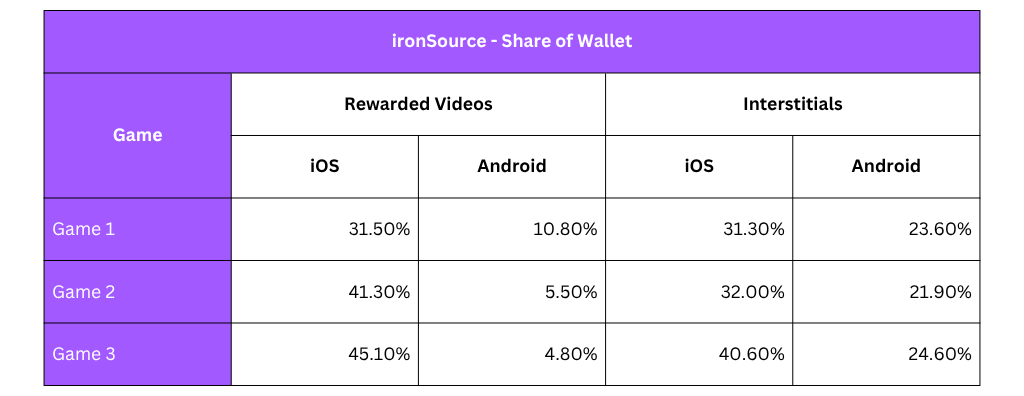

Let’s see what this looks like in practice. We analyzed COPPA traffic for 3 games that we’re managing. We compared the data from 1st to 29th April with that from 1st to 11th May, for both platforms, rewarded videos, and interstitials. We wanted to show the importance of ironSource's direct demand for these users, so we checked ironSource’s share of wallet and the shift we saw in the eCPM.

As you can see, ironSource was indeed a very important partner for monetizing COPPA users. Sure, other networks will take over the impressions or at least most of them, but how will that reflect on the ad revenue? Let’s see what happened to the eCPMs.

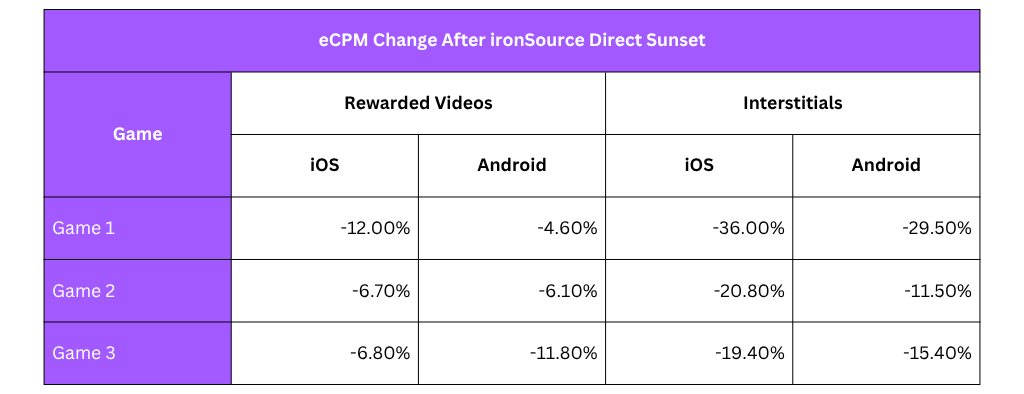

A decrease in the eCPMs from 6% to even more than 30% is a major hit. Important thing to note here is that there were no other significant changes in the setup or user distribution that would impact the eCPMs. So what happened?

ironSource was a top network for all these games. Once it shut down, other networks started picking up the impressions. Most of these networks already had lower eCPM than ironSource. They are now generating more impressions, meaning that their eCPM will become even lower. And in addition to that, getting ironSource out of the picture lowered the competition for each impression, which also leads to lower eCPM.

If there are some networks from the previous list that you weren’t testing, you should do it as soon as possible.

Regulatory pressures that keep coming

Besides the Children’s Online Privacy Protection Act (COPPA), every now and then, we hear about new regulations that might come into place. A recent regulation in Texas is a prime example. It demands that publishers split users into specific, granular age categories rather than just a binary "over/under 13." The Texas "App Store Accountability Act" (SB 2420) aims to impose a comprehensive age-verification system for all users and mandates that minors (under 18) obtain verifiable parental consent before downloading apps or making in-app purchases. Furthermore, it obligates app stores to pass "age-range signals" to developers and requires developers to assign age ratings to their apps and notify the store of any "significant changes" to their product's functionality. As of May 2026, SB 2420 is currently on hold. Texas is not an isolated case. Several other states have passed nearly identical "App Store Accountability" laws:

- Utah (SB 142): Set to go into effect on May 6, 2027, but currently facing similar legal challenges.

- Louisiana (HB 570): Scheduled for July 1, 2026, with mandates for age-gating and signal sharing.

- California: Their version is set for January 1, 2027, including a grace period for existing accounts.

Across the ocean, the UK brings its own regulations. Under the Online Safety Act, Ofcom now mandates "Highly Effective Age Assurance", meaning simple age-gate tick-boxes are being replaced by methods like facial age estimation. Simultaneously, the ICO’s Children’s Code forces a brutal choice: either implement these friction-heavy checks to prove a user is an adult, or apply child-level privacy protections to your entire audience by default. With multi-million-pound fines already being issued to major platforms in early 2026, the message is clear—if you can't verify them, you can't monetize them.

Developers and advertisers should consider this the warning shot: a growing wave of country-level and even US state-level protections for minors is already in the works, signaling a permanent shift in how the industry handles younger audiences. While Apple and Google are currently disputing these types of mandates in the US, they actually prepared technical frameworks to meet the requirements. Google Play released Play Age Signals API and Apple released Declared Age Range API and Significant Change API.

Even though there weren’t any specific mentions of any requirements for playing ads within the apps, if the age tracking system and enforcement changes, it will impact the ad monetization directly. If this becomes the standard, the technical burden and the full accountability will fall on publishers.

Why would new regulations drastically impact ad monetization performance?

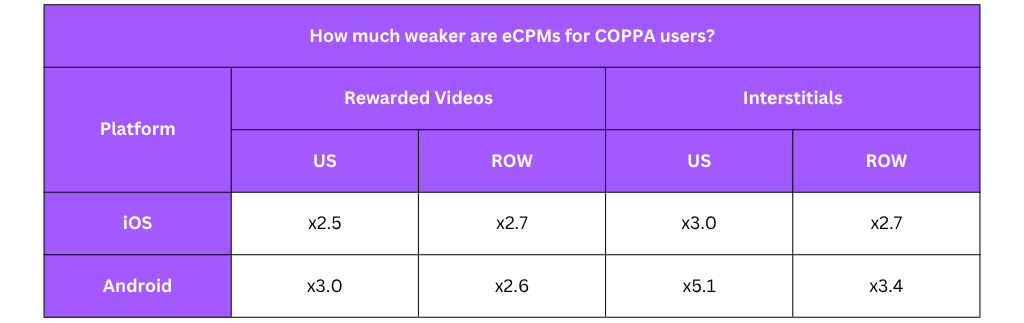

Because COPPA users (or any underage users if the regulations change) have an eCPM on a different scale of magnitude.

In the table below, you can see how many TIMES eCPM is lower on COPPA traffic compared to non-COPPA. So, we are not talking about 10%, 20%, or even 50% differences. We are talking about 2.5 to more than 5 times lower eCPMs.

If any of these regulations, COPPA included, start being enforced actively, publishers will have to split their users properly and monetize each segment accordingly. Just stating that the app is for a general or mixed audience and treating all users the same won’t be an option any longer.

The end of the general audience monetization strategy

We are witnessing the final days of the "general audience" ad monetization. When you combine the blockade of COPPA users on MAX with the bidding restrictions on AdMob and the disappearance of ironSource direct demand, the message to publishers is clear: ad monetization of COPPA users is hanging by a thread.

The data from the ironSource sunset confirms that the pool of COPPA-compliant demand is not just getting smaller, it is becoming less competitive and more fragmented. Furthermore, the shift in regulations that are happening in US states, the UK and beyond signals that similar regulations can easily become a new trend across the globe. This isn't just a hurdle for "kids' games", it’s a fundamental change for any developer with a mixed audience.

Awareness is the first step, but being ready to adapt to new conditions and change your mediation setup accordingly is what will ultimately determine your ad revenue in this new era.

The island is shrinking. Make sure you have a lifeboat ready.